Why higher prices are needed to develop ex-China rare earths supply

Western governments are starting to pledge meaningful funding for rare earth projects outside of China – but the biggest challenge will be the need for higher prices, according to Benchmark.

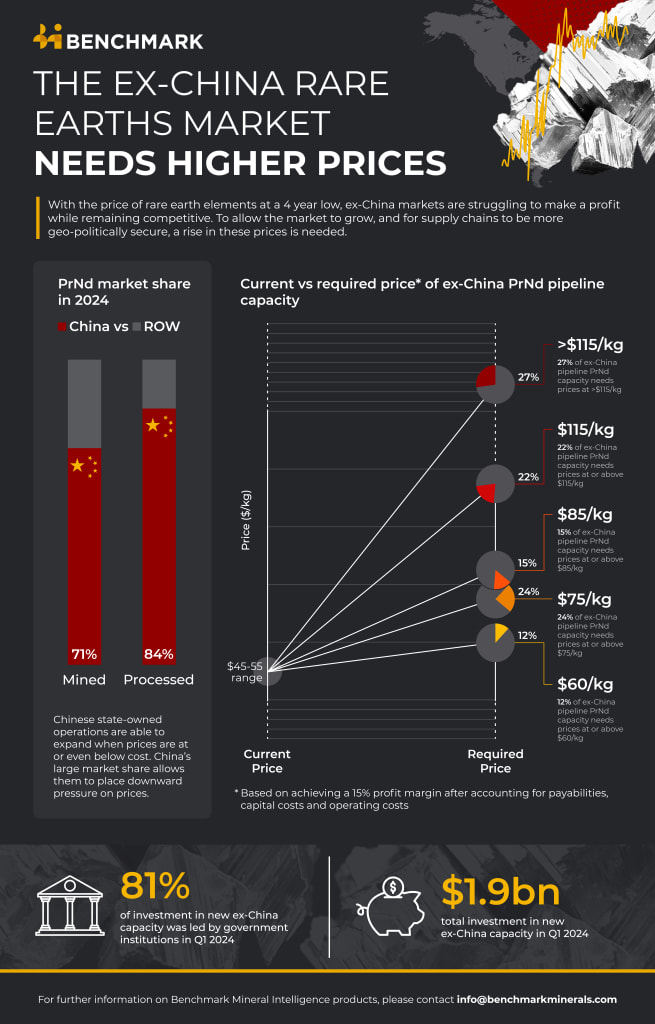

In the first quarter of this year 81% of investment in ex-China rare earth projects came from Western governments. In March the Australian government agreed to provide $533 million in 15-year debt funding to Arafura Rare Earths, which is developing the Nolans project in Western Australia to produce neodymium-praseodymium material for magnets used in electric vehicles.

Yet at the same time rare earth prices have fallen to four-year lows, due to expansion of supply in China and Myanmar. Prices for neodymium-praseodymium oxide is currently at $54 a kilogram in China, according to Benchmark’sRare Earth Price Assessment. Similarly, dysprosium oxide prices in March were recorded at $273kg.

At current rare earth prices no planned rare earth projects outside of China can achieve a 15% return on investment, according to Benchmark’s Rare Earth Forecast. Almost 40% of pipeline ex-China rare earth mines require prices of between $75/kg to $85/kg, according to Benchmark. 15% of this pipeline requires even higher prices, at above $85 a kilogram.

“Prices right now are simply too low for the ex-China market. There is great policy support from USA and Australia, but ex-China realised prices need to grow, or the economics of these assets needs to be otherwise augmented for the market to develop, and for critical mineral supply chains to be more geo-politically secure,” Daan De Jonge, an analyst at Benchmark, said.

“More needs to be done if you want to diversify the supply chain – OEMs need to accept that higher prices are required outside of China, or governments need to step in.”

Investment needed

Governments provided the bulk of the $1.9 billion invested in ex-China rare earth projects in the first quarter, according to Benchmark.

Yet, governments cannot provide all of the funding needed to make even a small dent in China’s dominance. And private capital will require the prospect of investment returns.

China’s share of refined rare earths is set to fall to only 77% by 2030, according to Benchmark, compared to 81% this year, while its share of mined supply is set to fall to 60% from 71% currently.

In terms of magnet materials China accounted for 83% of PrNd output last year, according to Benchmark.

And about 49% of the rare earth concentrate supply this year is set to come from just one mine – the Bayan Obo in Inner Mongolia.

China also produced 99.9% of global processed dysprosium last year.

Adding to the difficulties for Western miners is the fact that Chinese mines have also been ramping up supply, despite lower prices. Beijing announced a third rare earth mining and smelter quota in late 2023, rather than the normal two per year. As a result, the PrNd market is expected to be in a surplus out to 2026, according to Benchmark.

Competing on costs

Competing with Chinese costs is particularly hard for Western rare earth mines, according to de Jonge. Benchmark estimates that $60 a kilogram is a rational resistance price within China, but there are ways to support companies within China when their fundamental commodity price is too low.

“This dynamic exerts downward pressure on prices, below a ‘rational’ point,” he said.

One ex-China source of supply will be Lynas’ expansion at Mount Weld mine in Western Australia, forecast to contribute 3.1% of global mined PrNd supply in 2024, according toBenchmark’s Rare Earths Forecast. Yet this expansion may need prices as high as $95 a kilogram, according to de Jonge.

In addition, for another magnet rare earth, dysprosium, around a third of global supply is mined in Myanmar, where costs of production can be as low as $4 a kilogram, according to de Jonge.

“They’re still making a 70% margin at these low prices,” he said.

One aspect that may support ex-Chinese rare earth mines is sustainability, however.

Sustainabilityadvantage

Benchmark data shows that no Chinese rare earth miners reach “good practice,” in terms of their sustainability performance, compared to 100% of mining companies in Australia who reach this grade.

According to Benchmark’sRare Earths Sustainability Index, the sustainability performance of Chinese companies currently producing in both mined and refined rare earths industries is forecasted to remain relatively stagnant until 2040, with most companies classified as “Moderate Visibility.”

The Sustainability Index evaluates the extent of ESG transparency among rare earths companies and their commitment to best practices related to the most relevant and pressing Environmental, Social, and Governance concerns.

Each company has been tiered using Benchmark’s threshold methodology into 4 ranks from “Industry Leading”, “Good Practice”, “Moderate Visibility” to “Limited Visibility”.

OEM offtakes

As a result of China’s dominance of rare earths and related sustainability concerns, non-Chinese OEMs are already showing their interest in securing offtakes for rare earths – which may help support ex-China projects if prices are fixed in offtake agreements.

Benchmark expects the ex-China rare earth pipeline to grow as a result, even despite the headwinds.

Arafura Rare Earths has secured offtakes with Hyundai and Kia, as well as wind turbine producer Siemens Gamesa. It is targeting having 85% of its planned production from the Nolans project committed via binding offtake agreements, up from 53% currently.

And US rare earth minerMP Materialssigned a long-term supply agreement with General Motors in 2021. MP Materials will supply U.S.-sourced and manufactured rare earth materials, alloy and finished magnets for the electric motors.

“If you want an ex-China market this is exactly what’s needed,” de Jonge said. “You need investment when prices are low. You’ve got to pay up if you want the non-China pipeline to exist.”

Benchmark’s new Rare Earths Price Assessment provides price transparency for four rare earth elements along with market analysis every month.

It further expands our coverage of the rare earths market alongside our Rare Earths Forecast and ESG Report.

To request a sample report and learn more about our new Rare Earths Price Assessment coverage, please provide your details and our team will contact you shortly.

>

>  >

>  >

>  >

>  >

>  >

>  >

>