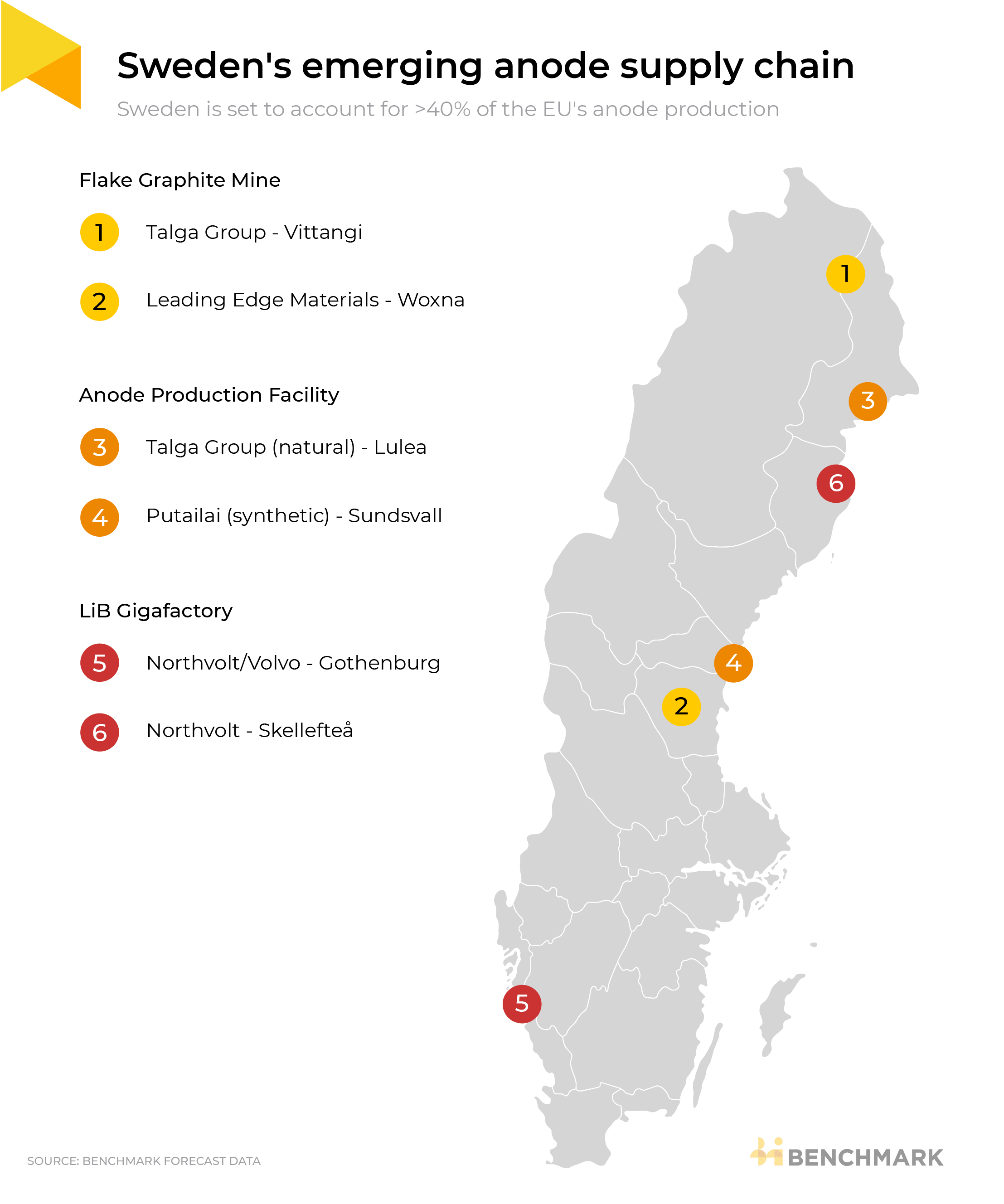

Europe’s anode supply chain converges on Sweden

Sweden is emerging as the leading hub for Europe’s battery anode value chain, as part of a broader trend of midstream battery investments converging around mineral-rich countries in Scandinavia.

Since the EU’s Critical Raw Materials Act (CRMA)mandated that at least 40%of the bloc’s consumption of critical raw materials be processed in Europe,projections for Sweden’s 2030 anode productionhave risen 132% year-on-year.

Last year, China’s ShanghaiPutailai announced it planned to build Europe’s largest anode productionfacility in Sundsvall, Sweden. The leading anode player is targeting a nameplate capacity of 100,000 tonnes per year of synthetic graphite anode materials. Talga Group is also planning on 104,000 tonnes per year of natural graphite anode capacity across multiple sites in Sweden, with first production from its 19,500 tonnes per year plant in Luleå scheduled for 2024.

These developments have seen Sweden set to account for over 40% of the EU’s anode production from 2028 onwards, according toBenchmark’s Anode Forecast. Neighbouring Finland has also benefited from a slew of anode related investments, as the two countries combine for 76% of the EU’s total planned anode capacity.

Logic of localisation key to investments

The economic benefits of vertical integration is underpinning this trend.Sweden is the only EU member stateset to produce spherical graphite material through to 2040

Talga Group’s spherical graphite production facility in Luleå is set to be first vertically integrated anode producer within the EU. The companybroke ground on Europe’s first anode plant in October 2023, later integrating supply from its own mine once in production.

Alongside meeting the CRMA’s extraction requirements,China’s recent graphite exports restrictionshas underscored the benefit of access to locally sourced feed.

“Theserestrictionshave increased attention from downstream players to the importance of supply diversification and sourcing material from ex-China markets,” said Tony Alderson, anode analyst at Benchmark.

The draw of Sweden is also close proximity to Northvolt’s European operations. Puitali’s facility is slated to begin producing anode material for the Swedish cell manufacturer once in production in 2025, while fellow anode entrants in the region are targeting Northvolt as a key customer for their material.

Sweden offers improved sustainability credentials

Sweden’s energy mix offers further incentive for midstream investment in the region. Renewables accounted for 67% of its grid in 2023 (compared to an EU average of 22%), the majority of which is hydroelectric power.

This is particularly pertinent for anode producers using synthetic graphite as feed, asthe Benchmark Graphite ESG Reportindicates that in China anode production from synthetic graphite is on average 83% more carbon-intensive than its natural graphite peers.

“Producing anode material from synthetic graphite is a carbon-intensive process and suppliers are under increased scrutiny from customers over their energy use,” said Alderson. “Sweden’s hydro-electric power offers anode players a way to introduce renewables into their production process.”

A close proximity to downstream customers in Europe would also considerably reduce the carbon emissions linked to transportation, when compared to shipping material from China.

Supply overhang spooks investors

Despite a wideningdisconnect between Europe’s anode supply and demand, the global oversupply in the anode market is hamstringing new investment in Europe.

The anode market is set to sustain a structural surplus until 2029, although much of the excess capacity in China is supply targeted for energy storage system markets – according toBenchmark’s Anode Forecast.

“Anode players in Europe are finding it hard to drum up new investment for expansion plans, as the structural oversupply in China scares off investors,” said Alderson.

To dateanode priceshave experienced double digit declines year-on-year across the board, as excess capacity in China has led producers to target lower-value end use markets in order to retain market share.

Benchmark provides independent price assessment and forecast for anode as part of our leading market intelligence covering the lithium ion battery to EV supply chain.

For further detailed insight into Benchmark’s battery cell coverage, please provide your details here and our experts will be in touch with you soon.

>

>  >

>  >

>  >

>  >

>  >

>  >

>  >

>