Will Rio Tinto’s move entice other mining majors into lithium?

For the last decade the world’s largest mining companies found the lithium sector not attractive enough to invest, given the relative geological abundance of the metal as well as small size and low barriers to entry.

We previouslydiscussedthat it was probably too late for major miners to enter the industry for value – unless there was a counter-cyclical move during the low part of the price cycle.

Such a move has now been made by Rio Tinto, withtheir $6.7 billion cash offerfor Arcadium Lithium, which has mines in Canada, Argentina and Australia.

After the merger between Allkem and Livent, Arcadium was very likely a target for several players. Nobody can discard a competing offer, but at 90% premium the likelihood is probably low.

Glencore is probably the only other major with some intention to play in the lithium market via recycling and prepayment offtake – albeit at a very small scale for now.

The rest of the pack (BHP, Anglo and Vale) remain firmly on the fence.

But Rio Tinto’s deal should provide a good reference for the corporate teams at these majors to refresh their own industry attractiveness profile and the potential pathways to enter the industry.

Changing dynamics

We argued in aprevious piecethat a “geology-first” approach was too simplistic for nascent, ultra-high-growth commodities such as lithium for which supply is likely to remain constrained by ex-China processing capabilities.

So apart from a price crash what else has changed over the last two years?

The short answer is not much: supply side constraints in the long run plus a steep cost curve will enable strong returns for players at the bottom end of the cost curve.

An additional tailwind for Rio’s move includes regulation and geopolitics creating the need for an “ex-China” supply chain to feed the batteries Western countries will consume and manufacture.

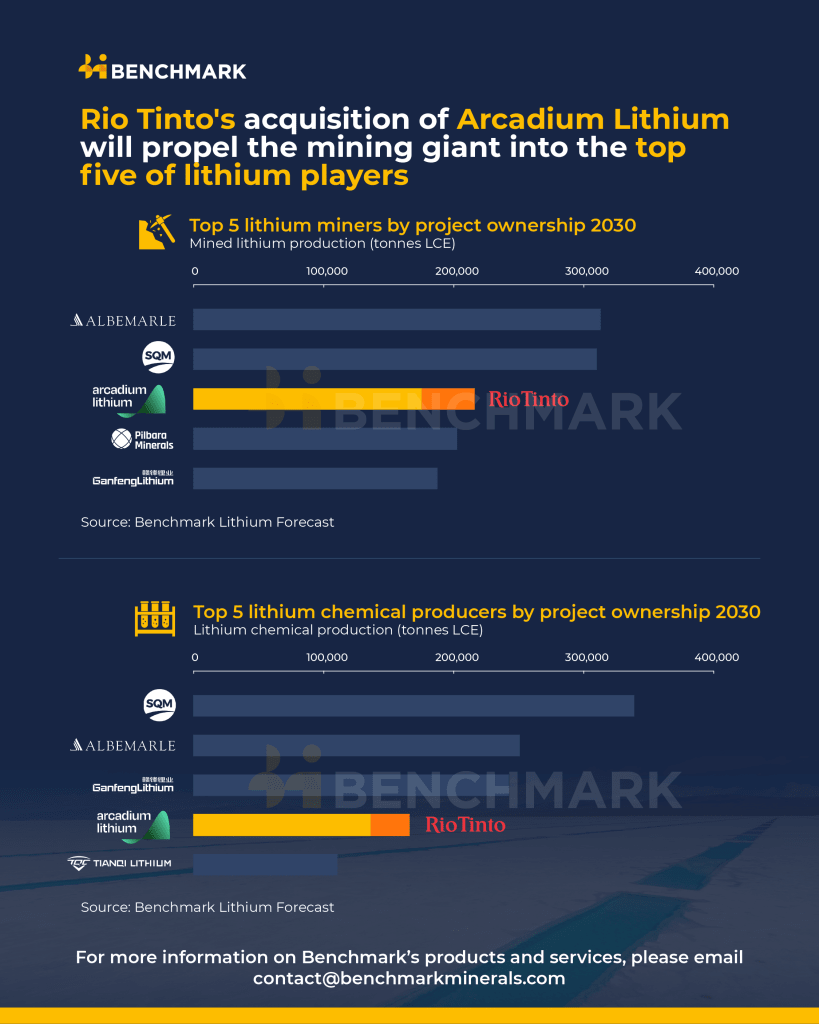

As highlighted by Benchmarkrecentlythe deal gives Rio the top third position in lithium globally. As the premium paid for Arcadium is almost 100%, some commentators are raising concerns of overpaying – some even referring to Rio’s poor M&A track record (Alcan, Riversdale) which led to massive write downs a decade ago.

However, those deals were made in a different context. This time Rio has taken time to learn about the industry via its development assetsJadarandRincon– hoping to get a low cost entry. The Arcadium move appears to have been pursued with the usual detailed industry and asset analyses large miners use in their investment decisions.

Ultimately the deal will be judged not on size or tonnage, but on value to shareholders.

Combining Benchmark’s proprietarylithium cost modeland $7bn deal value agreed, we estimate that the underlying lithium price required for the existing operating output (inclusive of brownfield expansions) to achieve a 15% IRR is likely to be $20,000 to 22,000 per tonne LCE. Benchmark’sLithium ForecastReport sets the long term price at $21,000 a tonne, right in the middle of this range.

The reality is that Rio is also buying a significant project execution risk as Arcadium has a strong list of development projects (Hombre Muerto expansions, Sal de Vida, Cauchari, Galaxy) which combined with Rio’s Jadar and Rincon projects account for about 280 to 300 ktpa LCE of additional capacity.

This level of expansion may stretch Rio Tinto’s execution capabilities. However, the good news is that most of those projects (with the notable exception of Galaxy) appear well positioned in Benchmark’s cost curve datasets so they would be able to absorb the usual cost increases and delays.

Will others follow?

The deal should provide much food for thought for the other big miners: there is no shortage of assets, but they all have their own challenges plus there is a need to have a strong integration push to achieve meaningful scale.

Rio Tinto’s presentation highlighted the potential synergies from combining a technology portfolio as well as regional footprints between the Arcadium assets and Rio’s legacy portfolio.

We can only speculate on what other majors might do, as some do have strong regional footprints in lithium rich regions e.g. Vale in Canada and Brazil and BHP in Australia and South America. However, both majors appear to have limited exposure to the processing technologies required to enable good operating performance.

>

>  >

>  >

>  >

>  >

>  >

>  >

>  >

>