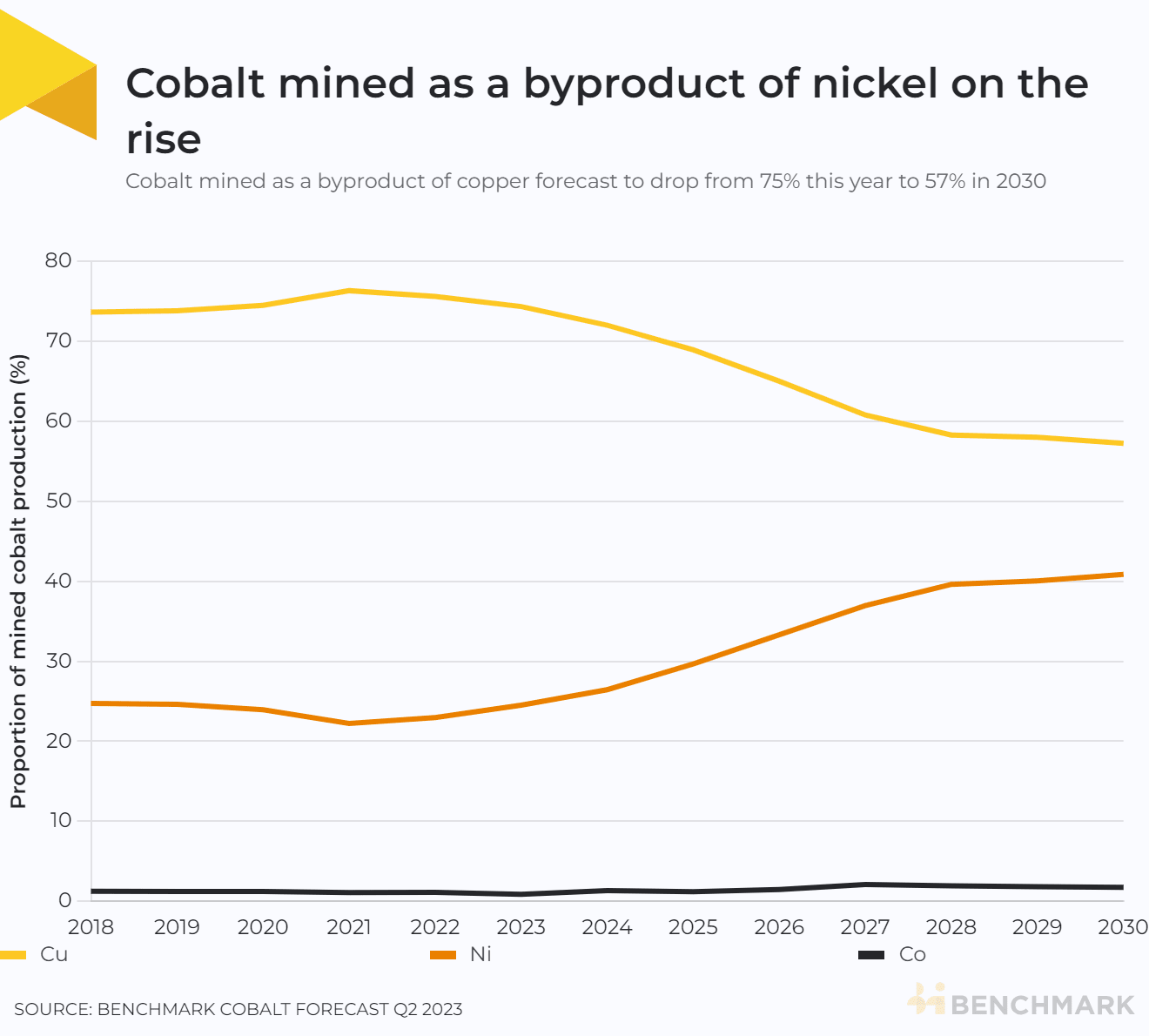

Two-fifths of cobalt could come from nickel mines by 2030

The proportion of global cobalt supply that is mined as a byproduct of nickel could increase from 25% this year to 41% in 2030, driven primarily by the riseof production in Indonesia, according toBenchmark’s Cobalt Forecast.

The majority of cobalt is currently mined as a byproduct of copper, with this accounting for three-quarters of this year’s forecast cobalt production. This could drop to 57% in 2030. This form of cobalt production almost entirely takes place in theDemocratic Republic of Congo(DRC).

Although Benchmark’s Cobalt Forecast shows that the cobalt market is currently oversupplied, a structural deficit is forecast from 2027 onwards meaning it is key thatnew supply planned in Indonesia comes online.

But cobalt supply is not in the hands of the cobalt market, rather it is at the whims of copper and nickel mining, which it is a byproduct of.

“If you don’t understand the copper and nickel markets, you don’t understand cobalt,” Piotr Kulas, an analyst at Benchmark, said.

Just 1% of cobalt mined this year will be the primary product of the mine from which it is produced, according to Benchmark’s Cobalt Forecast.

Different forms of cobalt

Cobalt produced from a copper mine is in the form of a copper-cobalt oxide. The two are separated through a sulphuric acid leaching process which produces cobalt hydroxide that is then shipped to China for conversion into cobalt sulphate for batteries.

The rise in cobalt production from nickel mines has been enabled by the high pressure acid leaching process (HPAL) which produces a mixed hydroxide precipitate (MHP) containing nickel, cobalt and manganese hydroxides. This is then converted into sulphates for batteries primarily in China.

Indonesia is the largest country for this kind of production. In 2030, Benchmark’s Cobalt Forecast shows the country could represent 82% of cobalt produced through the HPAL process. Australia and Papua New Guinea are forecast to represent 7% and 4% of the HPAL cobalt production in the same year.

Indonesian cobalt production has risen on the back of the country banning the export of nickel ores in 2020. This led to an uptick in HPAL project investments, primarily by Chinese companies, increasing the amount of cobalt produced as a byproduct.

Another driver for the rise of Indonesian cobalt is increasing concerns from automakers over the challenges associated with the DRC.

“Thecountry experiences constant logisticaland power issues, and responsible sourcing from theartisanal sectoris abig concern for many market players,” Jorge Uzcategui, an analyst at Benchmark, said.

Although Indonesia also has its own set ofenvironmental, social, andgovernance(ESG)concerns, there are reports suggesting that the country could get a Free Trade Agreement-like arrangement with the US, making critical minerals from the country potentially compliant with the Inflation Reduction Act.

Cobalt mined as a byproduct of nickel production also has the advantage of being produced in conjunction with other battery minerals. Kulas noted that the ratios of nickel and cobalt in MHP is similar to that required by NCM 811 cathode material, providing an advantage over cobalt sourced from the DRC which requires separate sourcing of nickel and manganese feedstocks.

But with the cobalt market forecast to enter a deficit from 2027, supply is needed soon and the DRC has the advantage of being a more mature producer and higher cobalt grades.

“One of the most significant aspects of this shift is that the cobalt market will become slightly more diversified,” Uzcategui said.

Cobalt’s unique pricing dynamics

A consequence of cobalt being mined as a byproduct of other metals is that supply and price are not as intimately connected as is the case for other battery metals.

“A good example of this is that right now,cobalt hydroxide is at the lowest it has been in the last five years, though, despite that, cobalt mining isn’t slowing down at all,” Roman Aubry, an analyst at Benchmark, said.

Aubry suggests that a rise in the prevalence of cobalt produced as a byproduct of nickel mining, could call for greater standardisation in fledgling MHP cobalt payable pricing.

“That being said, since cobalt in MHP is such a small amount, it still very much takes a backseat to nickel in MHP,” he said.

Benchmark provides a range of prices, data and market intelligence services for the nickel and cobalt markets:

To learn more about any of these services and to speak to our experts, please provide your details here:

>

>  >

>  >

>  >

>  >

>  >

>  >

>  >

>