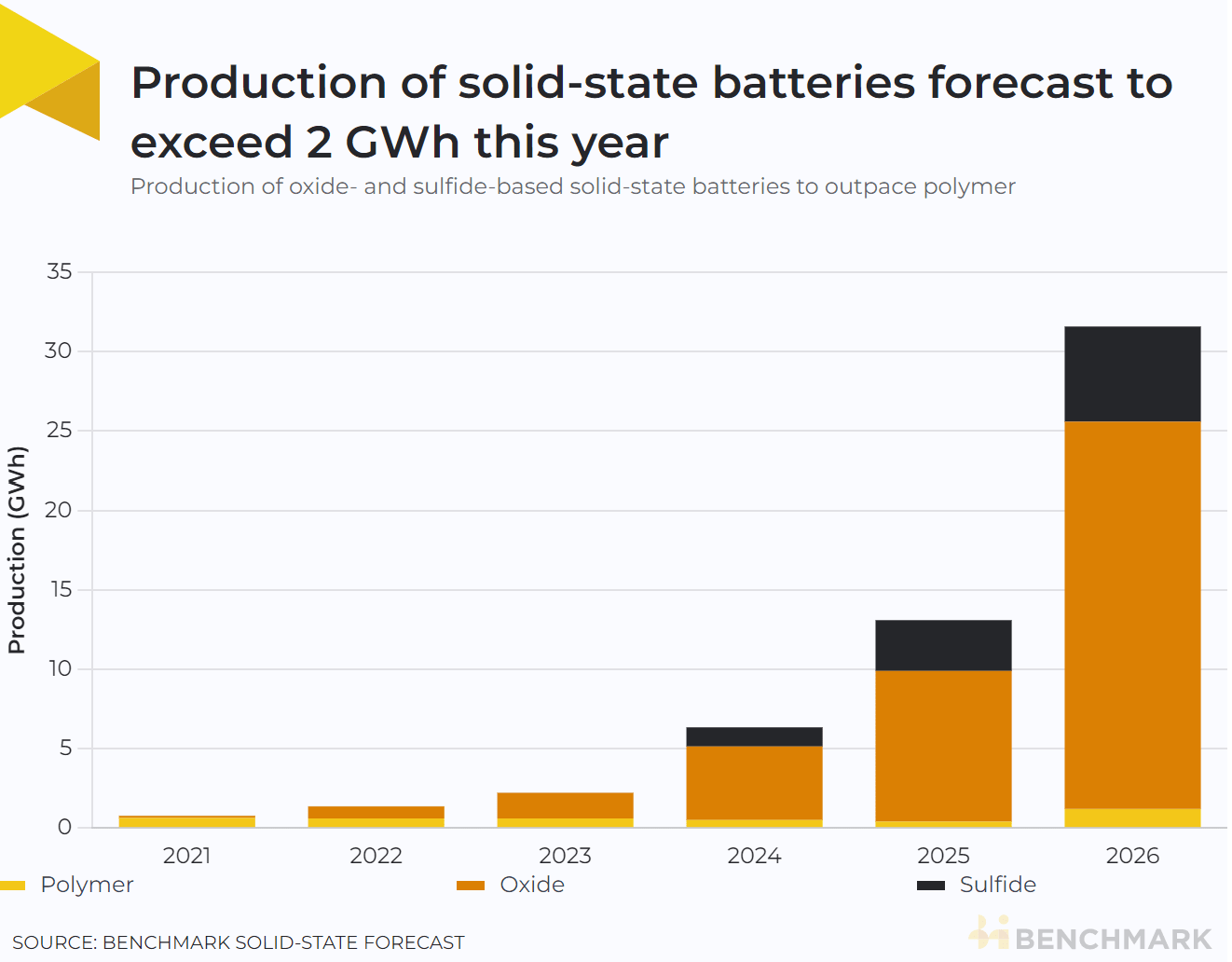

Solid-state production forecast to hit 2 GWh this year as oxide batteries dominate

This year is set to see solid-state battery production exceed two gigawatt-hours for the first time, according toBenchmark’s Solid-state Forecast.

A solid-state battery replaces the liquid electrolyte used in traditional lithium ion batteries with a solid-state separator. The composition of this can be broadly divided into polymers, oxide-, and sulfide-based solid electrolytes. This year, 73% of solid-state battery production is forecast to use an oxide-based electrolyte, with polymers accounting for the other 27%.

By enabling the use of next-generation cathode andanode materials, solid-state batteries have the potential to achieve higher energy densities whilst also improving safety by eliminating the flammable liquid electrolyte component.

“Over the past 12 months, the solid-state and lithium metal battery markets have really taken off.Annual production surpassed one gigawatt-hour at the start of the year, and since then many producers have made significant steps towards formalautomotive qualification.” Rory McNulty, an analyst at Benchmark, said.

Polymer solid-state

To date, only polymer-based solid-state batteries have successfully been commercialised for use in electric vehicle applications.

In 2016, Blue Solutions, a subsidiary of France’s Bolloré Group, deployed its polymer-based solid-state batteries in electric buses through the company’s subsidiary BlueBus. The company has a production capacity of 1.5 GWh spread across France and Canada, with plans to ramp capacity to over 15 GWh by 2030.

“One of the key benefits of solid-state polymer electrolytes is that they have been demonstrated in an application: we know they work,” McNulty said, adding that robust supply chains and ease of manufacture are also key benefits of the chemistry.

However, these electrolytes often have poor ionic conductivity leading to low performance, and often require pre-heating to between 60 – 80 °C to be conductive enough to function, McNulty explained.

This isn’t a major issue for predictable drive-cycle applications, such as electric buses, as the batteries can be preheated in the depot before being deployed.

Currently, solid-state polymer electrolytes are not compatible with high-voltage cathode materials (e.g., high-nickel chemistries), though the next generation of solid-state polymer electrolytes may overcome this challenge, McNulty suggested.

Oxide solid-state

The ionic conductivity and performance of oxide-based solid-state electrolytes are higher than those of polymer-based electrolytes. This class of electrolyte ranks excellent in terms of electrochemical, thermal, and chemical stability, according to Benchmark’s Solid-state Forecast.

However, oxide materials are often extremely brittle, making them difficult to handle in the manufacturing process. The raw material supply chain is also complicated by the need forlanthanumand zirconia, both of which are non-trivial to source and are typically mined by-products, McNulty said.

China’s Ganfeng LiEnergy, a subsidiary of Ganfeng Lithium, last year announced plans to build a 10 GWh gigafactory in Chongqing, China, to produce oxide-based solid-state batteries.

Taiwan-based ProLogium is another major player in the oxide industry. Having formedpartnerships with several automakersincluding Nio and VinFast in Asia and Mercedes-Benz in Europe, the company is in the process of identifying a second gigafactory site in Europe or North America alongside scaling their domestic production capacity to 3 GWh in 2023.

QuantumScape, a US-based oxide-based solid-state battery developer, has the backing of Volkswagen and SAIC Motors. The company is currently in the pre-pilot stage of production and plans to build a 1 GWh pilot plant through a joint venture with Volkswagen, which could be operational from 2026.

Sulfide solid-state

The highest-performing solid-state electrolytes are typically in the sulfide family. These have extremely good ionic conductivity, sometimes exceeding that of liquid electrolytes. However, although considerable progress has been made in manufacturing the electrolytes, there is no announced commercial-scale production of battery cells at this time.

“The other advantage over the oxides that the sulfide have is the processability,” Josh Buettner-Garrett, chief technical officer of Solid Power–a sulfide solid-state developer–told Benchmark. “They’re somewhat malleable. So you can do things like taking pretty conventional calendaring lines, used in traditional lithium ion [production], and apply those same types of processes to these sulfide electrolytes.”

Solid Power, based in Colorado, US, is one of the most active players in the sulfide space. In June last year, the company established a pilot production line to develop its A-sample cells to send to automakers for qualification. The company has partnerships BMW and Ford.

One of the key raw materials for sulfide-based solid electrolytes is lithium sulfide, which is one of the key bottlenecks to the commercialisation of the technology, as until now R&D has been the primary consumer, with no established commercial market.

“Lithium sulfide is the main supply chain challenge,” Buettner-Garrett said. “It’s really just the chicken and egg problem of how large of a scaling effort [of lithium sulfide production] can be justified.”

>

>  >

>  >

>  >

>  >

>  >

>  >

>  >

>