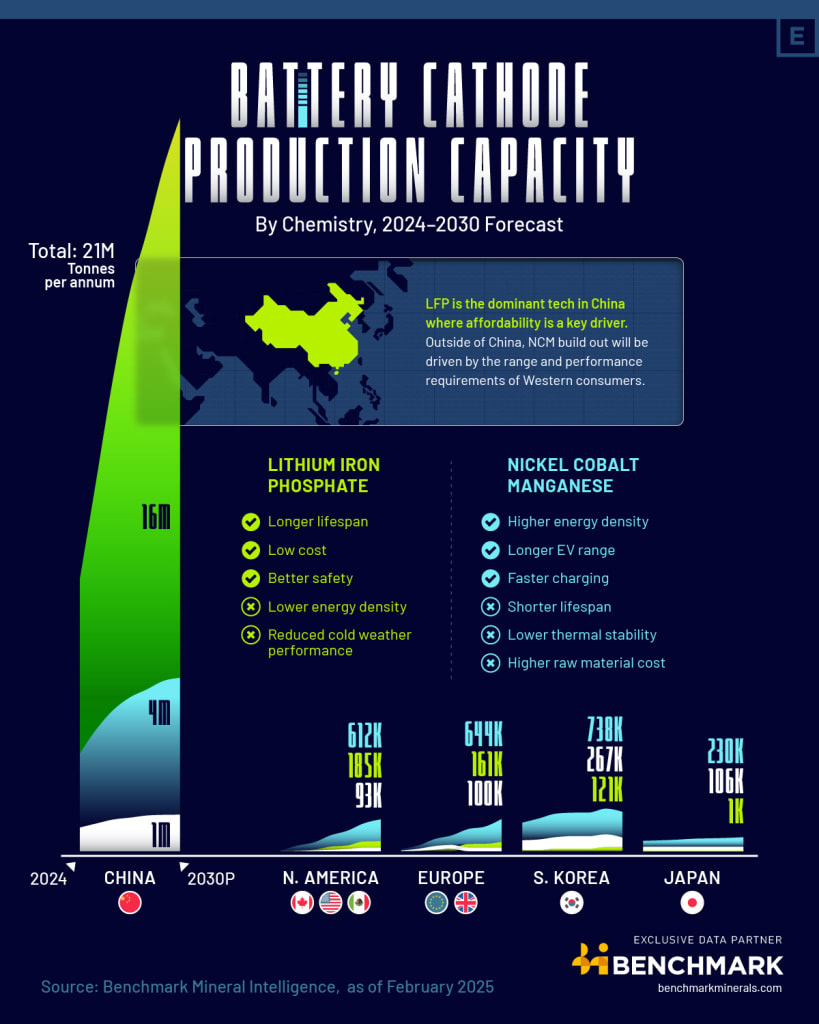

Infographic: Regional trends in cathode production capacity

Global cathode active material (CAM) production capacity is set to grow 178% between 2024 and 2030, asassessed by Benchmark.

The bulk of thiscapacity is in China, with the country accounting for 87% of capacity in 2024, falling slightly to 84% by 2030.

In China, the predominant cathode chemistry islithium iron phosphate(LFP) driven in part by the country’s appetite for cheaper electric vehicles. LFP is set to account for three-quarters of China’s CAM capacity by 2030.

Outside of China, the largest proportion of CAM production capacity is fornickel cobalt manganese(NCM) chemistries, at 60% in 2030. NCM chemistries are more suited to longer-range EVs than LFP, albeit at a higher cost.

North AmericaandEuropecurrently have low levels of CAM production capacity, but are set to see compound annual growth rates of 101% and 57%, respectively, between 2024 and 2030.

South Koreahas the largest CAM production capacity outside of China and is set to maintain this position with a 6% compound annual growth rate over the same period. South Korean and Japanese companies are focusing theircapacity expansions overseasin North America and Europe, more so than domestically.

Chart showing cathode active material (CAM) production capacity by region and cathode chemistry (green = LFP, blue = NCM, white = other)

The data in this article and infographic comes from Benchmark’s Cathode Price Assessment. To find out more, fill in this form below and one of the team will be in touch:

>

>  >

>  >

>  >

>  >

>  >

>  >

>  >

>