ESG of graphite: how do synthetic graphite and natural graphite compare?

Automakers are looking to reduce the carbon intensity of the battery materials they use for their electric vehicles, yet graphite presents a key problem for the industry.

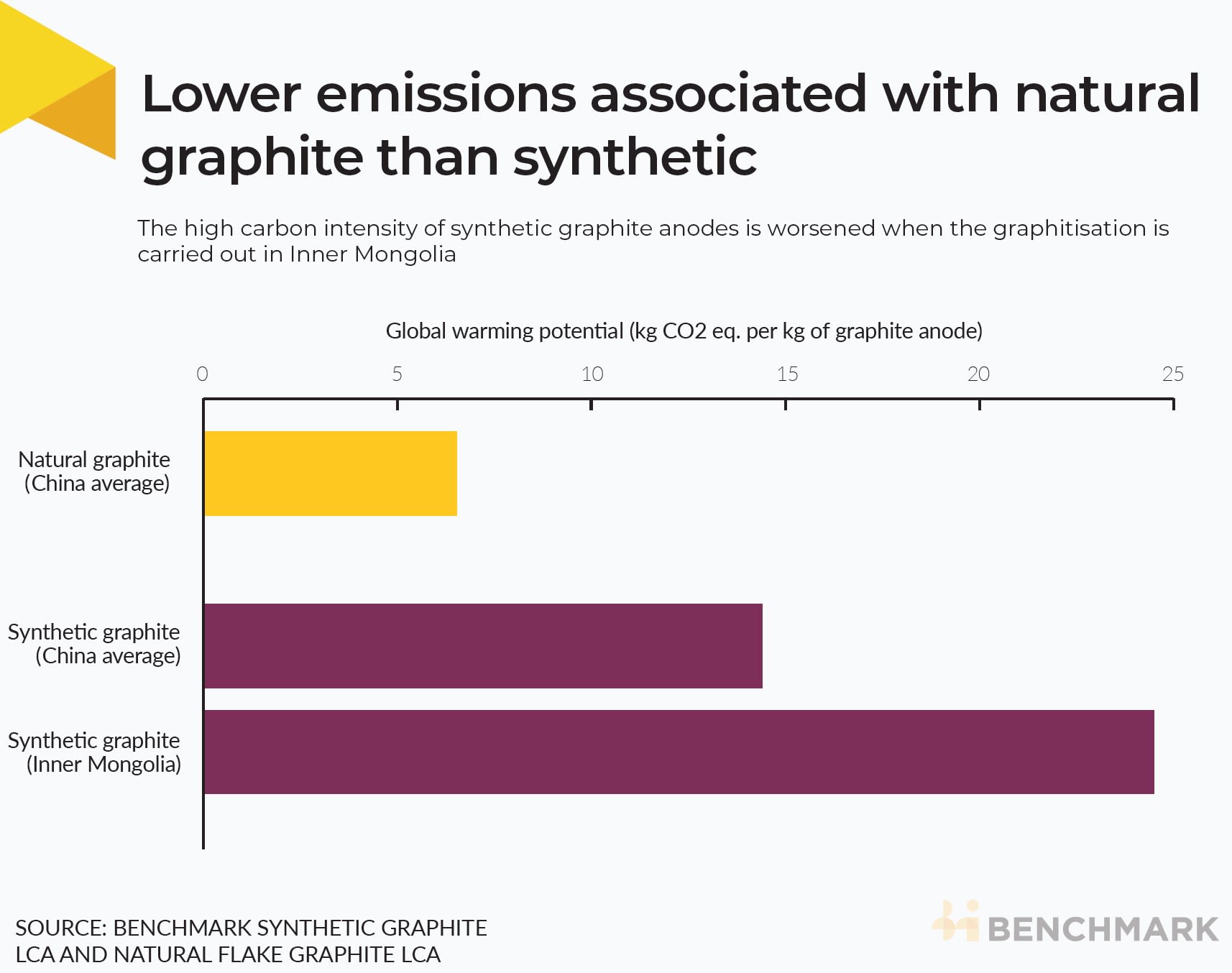

Synthetic graphite anode production can be over four times more carbon intensive than natural graphite anode production, due to its use of energy and fossil fuels as a feedstock.

Currently, most of the world’s lithium ion batteries use synthetic graphite, which is especially popular in China.

But both supply chains have multiple environmental, social and governance (ESG) concerns, with natural graphite subject to the risks of an ongoing conflict in northern Mozambique that started in 2017.

“Overall there is more fragility in the natural graphite supply chain at current than the synthetic supply chain,” George Miller, an analyst at Benchmark, said. “In the long term, however, the phase-out of fossil fuels poses a threat to the continued large-scale supply of coke to the synthetic graphite supply chain.”

Below we set out how the two graphite materials compare.

Synthetic graphite’s Inner Mongolia problem

The graphitisation of coke products into synthetic graphite requires the largest energy input. If fossil-based electricity is used for this process, then the carbon emissions increase substantially.

Notably, synthetic graphite production can be even more carbon-intensive if graphitisation takes place inInner Mongolia due to the use of coal-based electricityin the province.

Synthetic graphite is also dependent on the fossil fuel industry. The preferred feedstock is petroleum coke which comes from the heavy fractions left over from crude oil production. A cheaper, alternative feedstock is pitch coke, which comes from coal tar.

Natural graphite’s carbon footprint

The production of natural graphite anodes is around 55% less carbon intensive than the average synthetic graphite anode produced in China, as assessed by Benchmark’s synthetic graphite and natural graphite Life Cycle Assessments (LCA).

For natural graphite, two-thirds of the carbon emissions come from the spheroidisation process, for which China currently has a monopoly. Spheroidisation is the process in which flake graphite particles are mechanically rounded. This leads to the loss of some material, but yields improvements in the performance of the anode.

There are only 11 companies tracked by Benchmark looking to developspherical graphite (SPG) production capacity outside of China. The largest of these in the near term is Syrah Resources, which is developing 11,250 tonnes of SPG production capacity in the US, with the possibility of expanding this to 45,000 tonnes.

Natural graphite’s fragile supply chain

Although natural graphite is associated with fewer carbon emissions, it is not without its own ESG concerns.

China produced 68% of natural graphite last year, with most of this concentrated in Heilongjiang province,which shuts down for winter every yearas temperatures drop too low for machinery and personnel to operate.

Amajor source of natural graphite outside of Chinain the short term is Mozambique, which currently accounts for 10% of mined graphite, rising to 14% in 2030 according to Benchmark’s Graphite Forecast.

Benchmark forecasts 96% of Mozambican graphite in 2025 will be mined in northern Cabo Delgado province which, since 2017, has been the site of attacks from an Islamist State-linked insurgency group.

In June this year Triton Resources, an Australian-owned graphite miner, said that two of its staff were killed after an attack by insurgents. Syrah Resources also suspended personnel and logistics movements on a primary transport route in the province following the attack.

Nearly 70% of graphite mining in Europe took place in Russia and Ukraine. Although Volt Resources resumed their Ukrainian operations earlier this year, the war could impact the stability of Europe’s graphite production.

Madagascar is another alternative graphite supply to China, accounting for nearly 10% of supply today. However, the region suffers from cyclones, one of which halted operations at Tirupati Graphite’s mine in the country earlier this year.

Climate change has made these cyclones more severe and it is expected they will get more destructive in the future.

Learn more about Benchmark’s ESG services

To learn more about Benchmark’s ESG analysis services for cobalt, lithium, nickel and graphite, please fill out the followingform.

>

>  >

>  >

>  >

>  >

>  >

>  >

>