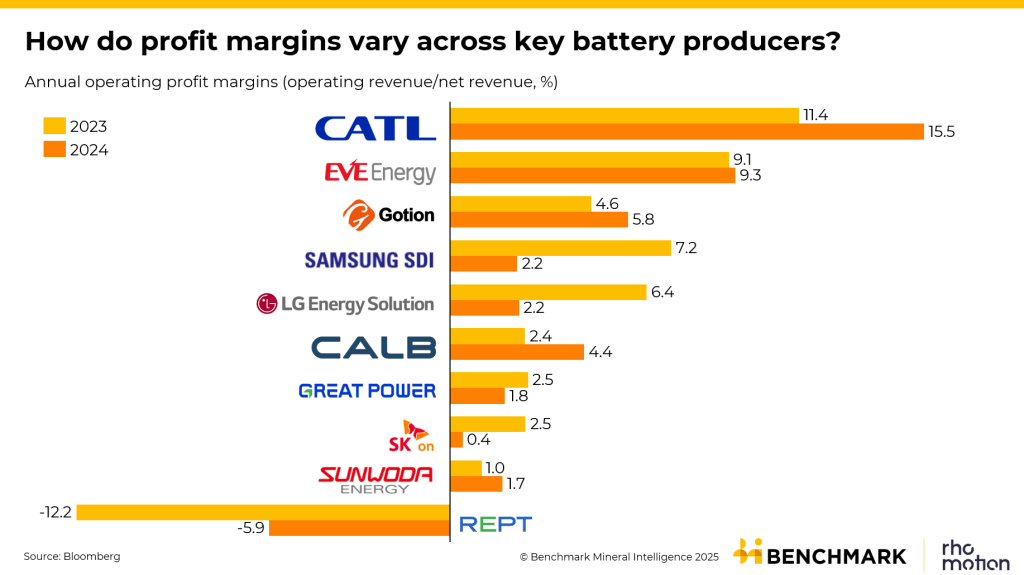

How do profit margins vary across key battery producers?

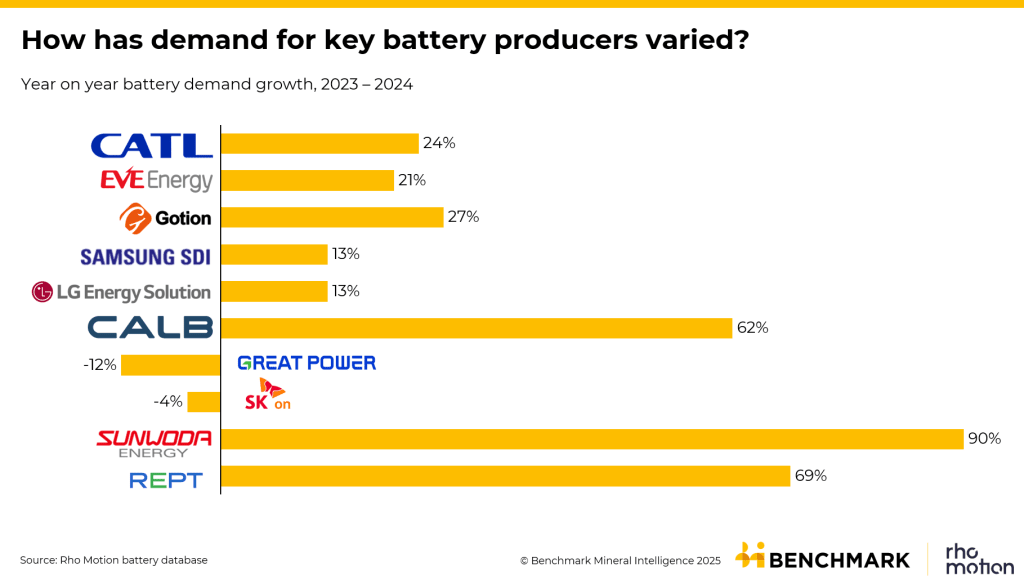

Battery demand has continually been growing over the last decade, withannual global battery demand surpassing 1TWh for the first time in 2024according toRho Motion’s Battery Demand Service. As battery demand has grown, cell prices have followed a downward trajectory with global weighted cell lithium ion cell prices now hovering above $60/kWh according toBenchmark’s Cell Price Assessment. These developments have in turn affected companies’ profit margins.

N.B. In this article the operating income ratio (operating income/revenue) has been examined. This figure is a reflection of the core profitability of battery maker’s operations as it indicates how efficiently each company turns revenue into operating profit after covering production and overhead costs.

CATL leads the way, but other Chinese players are seeing increases in margins

In 2023, CATL’s profit margin was 11.4%, in 2024 this increased to 15.5%. According to Rho Motion data,CATL controlled ~32% of the global battery demand market in 2024, underpinning how integral the company is to many EV and BESS supply chains. The scale at which it can its produces batteries helps it achieve strong operating profit margins. While CATL saw the largest jump in operating profit margin, many other Chinese battery makers also saw improvements including CALB, Gotion, Sunwoda, EVE Energy and REPT. This comes despite battery prices continuing to fall. The profit margin improvements are largely down to increased sales as players have expanded further into global markets, and improved production efficiencies but also local subsidies that reduce CAPEX and OPEX costs for Chinese players allowing stronger margins.

Ex-China battery makers see profit margins slip

Two of the largest ex-China battery producers Samsung SDI and LG Energy Solution saw their profit margins slip from 7.2% and 6.4%, respectively, each to 2.2%. In 2024, Samsung SDI and LG Energy Solution accounted for 4% and 13% of the battery market respectively. The fall in profit margins aligns with a decline in each company’s revenue, despite increasing sales volumes. As battery prices fell from 2023 to 2024, LG Energy Solution and Samsung SDI did not achieve sufficient sales growth to offset the drop in cell prices.

What is the outlook for profitability in the battery industry?

Battery cell prices in 2024 reached all-time lows, driven by improved production efficiency and falling lithium prices. While low cell prices have the potential to impact revenues and overall profitability, most major producers continue to operate with relatively healthy profit margins. The EV and BESS markets are expected to keep growing, providing consistent demand and allowing companies to expand sales and potentially absorb further reductions in cell prices. Additionally advances in battery technology and production efficiency could also aid profitability but also push cell prices downward.

However cell prices have remained relatively stable in the first quarter of 2025 and are anticipated to remain so in the near future, meaning margins in 2025 could remain more stable compared to 2023 or 2024.

>

>  >

>  >

>  >

>  >

>  >

>  >

>  >

>